What's in a NAV?

Net Asset What?

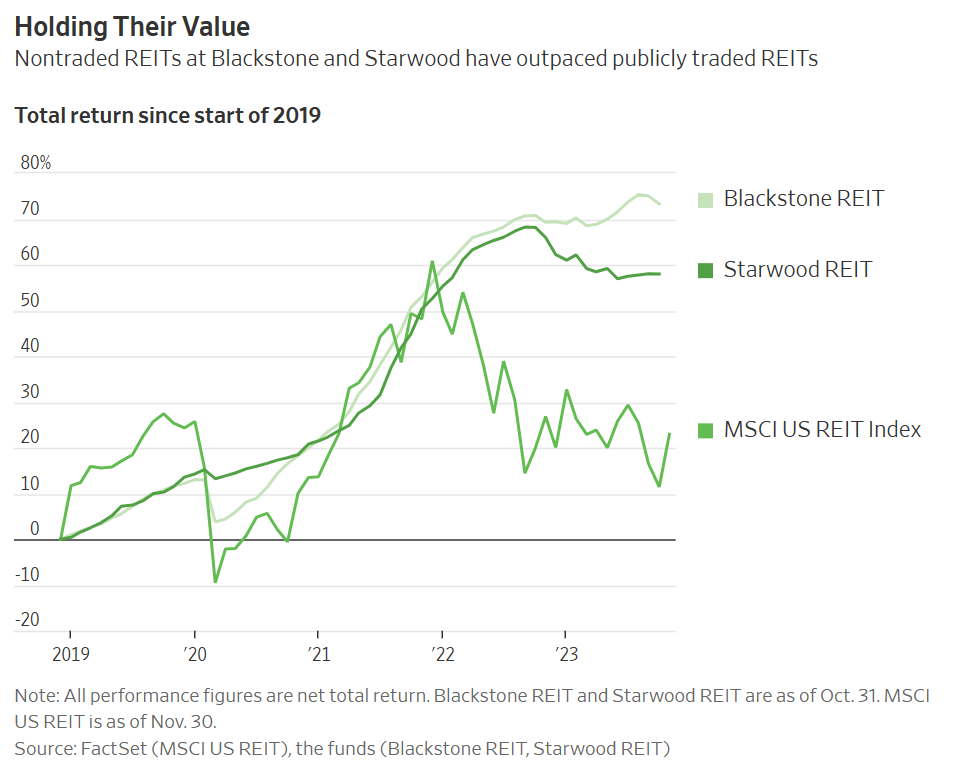

Non-Traded REITs Struggle to Explain Their Own Valuations

Non-traded REIT valuations were the focus of a Wall Street Journal report this week that states, "[i]n most cases the funds, known as nontraded real-estate-investment trusts, have broad leeway to define their NAV measurements however they want." The journal goes on to highlight the growing disparity between these funds' reported NAVs and the performance of listed REITs. Non-Traded REITs not only calculate performance based on their own NAV calculations, but they also sell shares and charge fees based on those assessments. Per the WSJ,

"According to fund filings, there are many adjustments nontraded REITs make to calculate non-GAAP NAV. Some don’t subtract all their liabilities. Some include fair-value gains and losses on their own debt; others don’t. Some update their real-estate assets’ values more frequently than others or rely more heavily on third-party firms to value them."

Investors can take little comfort in these funds' disclosures, as Blackstone, Starwood and others all state that they "calculate and publish NAV solely for purposes of establishing the price at which we sell and repurchase shares of our common stock, and you should not view our NAV as a measure of our historical or future financial condition or performance.” Many of these funds charge performance fees which are at least partially based on the performance reflected by changes in NAV. The same NAV that the funds explicitly say are not a measure of performance.

Non-traded REITs compound the issue of unclear valuations by gating redemptions and limiting liquidity. Some firms will purchase stakes directly from investors, but those transactions invariably happen at significant discounts to the stated Net Asset Values. John Cox of Cox Capital Partners, a secondary buyer of private REIT interests tells the WSJ,

"They should call it `price.’ They should say, ‘This is our price per share’ and just leave it at that.”

Well put John, we agree.

Our Residential REIT Strategy

The Big Ideas

Market Capitalization-driven REIT strategies do not create optimal portfolios

A large portion of REIT returns come from dividends

Residential REITs are fundamentally more suited to mean-reversion

One of Armada's core beliefs is that market capitalization-weighted REIT exposure does not create the best listed real estate strategy for investors. Because of the payout requirement, REITs are more like asset-heavy pass-through entities than traditional companies that can grow equity value through re-investing internally generated cash flows.

As a result, much of the return in REIT ownership comes from dividends. Further, how a REIT is capitalized is crucially important to its return, none of which is adequately reflected in a pure capitalization weighted portfolio. Going back 10 years, over 50% of total return in residential REITs has come from dividends not price appreciation.

When we began looking at ways to improve REIT investment strategies, we knew that alternative weighting methods and REIT-specific factors would be important considerations. It is a fair generalization to say that the equity of REITs is more volatile than the underlying assets. This may be exceptionally true for residential REITs where the consistent demand for housing supports generally rising rental rates. These fundamental characteristics make residential REIT equity more likely to experience mean reversion characteristics.

As an example, in the preceding 10 years, Mid-America Apartment Communities' valuation multiple (Price / Funds from Operation) has been far more volatile than the underlying cash flows.

As we back tested weighting residential REITs by various factors (FFO Yield, Dividend Growth, even Total Asset Value), we noticed that REITs with smaller market capitalization were contributing more to the overall return. There are a variety of explanations for this, some quantitatively driven like leverage ratios and others that were more macro-based like exposure to faster growing rental markets.

Ultimately however, it became clear that the best solution was simplest: Discretionarily equally weighting residential REITs generates a portfolio of listed real estate with a slightly higher dividend, more leverage and greater geographic diversity than a market capitalization weighted portfolio. Moreover, an equal weighted strategy is definitionally one that benefits from the mean reversion inherent to Residential REITs, as you sell large caps and buy small caps on quarterly rebalances.

For investors who believe in the long-term strength of the domestic rental housing market, we believe a proximally equally weighted basket off high-quality residential and residential-adjacent REITs is a more optimal strategy.

Quote Book

Carson Block of Muddy Waters Research

Carson Block of Muddy Waters Research Coming at the King 👑

“Even assuming rate cuts, [Blackstone Mortgage Trust] BXMT's losses on its $23.2 billion net book value of loans could reach ~$2.5 billion to ~$4.5 billion. BXMT's market cap, which is currently $4.0 billion, is at risk of being completely wiped out by these losses.”

- Carson Block, Muddy Waters Research (Muddy Waters)

Quality, Quality, Quality 👏

"Overall, we think quality will win out in every class in real estate.”

- John McCallion, CFO, MetLife (Bloomberg)

Multifamily Transition 🏠

“So first off, I think there was a lot of faith in the sector in lower for longer, too much faith, frankly, I'd believe. And now if you believe in a soft landing and higher for longer, that's a very painful transition. And the reason that's such a painful transition is cap rates or your yields historically have had a 200 basis point spread to the 10-year.”

- Lee Everett, Waterton (Bloomberg)