The Retreat from Private Real Estate

Pensions Trim Private Real Estate Exposure

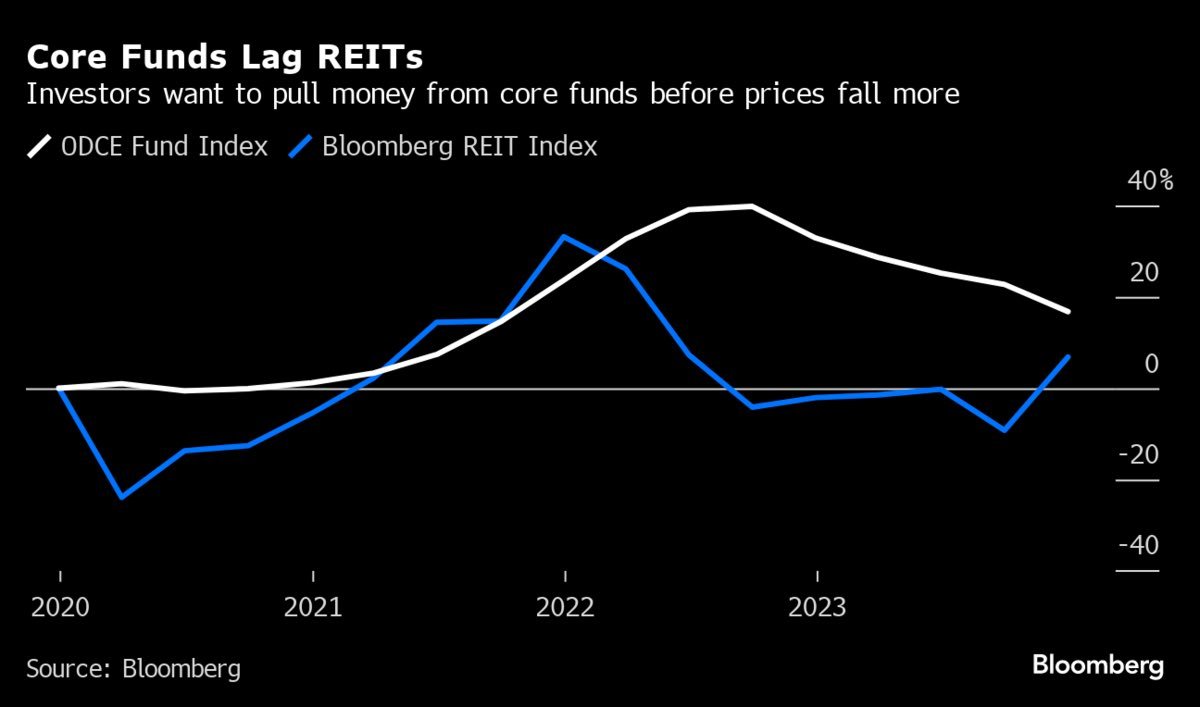

Pension commitments to real estate funds fell 50% in 2023 according to Green Street. New fundraising isn't the only issue, Bloomberg reports that redemptions from open-end funds are spiking as well.

"Investors sought to pull about $38 billion from open-end core real estate funds at the end of 2023, a nearly 90% jump from a year earlier, according to IDR Investment Management, which manages a fund that tracks an index of the investments."

The causes for the tepid appetite for real estate are two-fold. Foremost, there is a belief the private market has not fully digested last year's interest rate hikes and property values have further to fall. The other issue is that real estate strategies have been crowded out by higher yielding options like private credit.

Pensions, which focus on asset allocation, found themselves overweight real estate when the stock market fell in 2022, but now that equities are back at all-time-highs many are hesitant to rush back in to real estate commitments. "We want to see a sign of the bottom before we put more capital to work," Douglas Weill, co-managing partner of investment advisory firm Hodes Weill & Associates told Bloomberg.

Such extreme sentiment on the asset class usually signals an infection point. Scott McIntosh, a director at Chicago-based Ferguson, told Green Street ,“In terms of fundraising, we’re probably at the bottom.”

At Armada, we believe key benefits of listed real estate are not only its transparency, but also its liquidity. Public REITs typically lead private real estate values. In the context of this new private fundraising data, the macro-outlook for REITs is increasingly compelling.

Affordability, Supply & Rent Growth

Rent Burden Lightened for Median US Households Last Year

Moody's Analytics reports that rent-to-income (RTI) ratios have continued to moderate on a combination of slowing rent growth and rising wages.

"The national rent-to-income (RTI) ratio continued to moderate since it peaked in mid-2022, driven by higher-than-expected median income growth and deceleration in rent growth (with recorded declines for some areas). Still, metros previously identified as 'rent burdened' remained the same for this edition of the report, even as 85% of all metros experienced RTI decline relative to one year prior."

These high-level metrics conceal some more nuanced trends within both asset types and geographies. According to CBRE, the gap in rental growth rates "between the top markets – generally Midwest cities with little supply growth – and bottom markets – generally Southern cities with aggressive supply growth – is narrower than usual."

Stronger markets in Midwest are not able to push rent growth as aggressively, and despite supply challenges in the Sunbelt absorption has remained robust.

The Share of the More Affordable Market Segment Continued to Slip

Within product types, even though A-class units are experiencing higher vacancy rates, B/C units are structurally undersupplied. Moody's,

"Class B/C units typically rent for 30% less than Class A units, Class B/C units typically do not muster investor or developer interest for a variety of factors – including increasing building costs and perceptions of constraints on income generation...Class B/C units slipped from two-thirds in the early 2000s to less than half by the end of 2023."

We have been developing our proprietary Armada MSA Edge technology to link these trends to underlying REIT portfolios. We link real-time private market fundamentals to the capital allocation of REIT portfolios and use machine learning to uncover unintuitive relationships between this data and public REIT performance.

If you'd like to learn more about MSA Edge please reach out to hhopcroft@armadaetfs.com